隨著第四次比特幣減半的臨近,加密貨幣市場預計將迎來關鍵時刻。這起事件預計將在今年4月16日至20日之間發生,比特幣的礦工獎勵將從每區塊6.25 BTC減少一半,降至3.125 BTC。雖然歷史上的減半一直是潛在市場趨勢的關鍵指標,但由於先前三個事件的樣本量有限,Volcano X敦促在直接推斷過去的模式以預測未來結果時要謹慎。

This event is expected to take place between 16 and 20 April of this year, and will result in a 50% reduction in Bitcoins from 6.25 to 3.125 BTC per block. While the historical reduction has been a key indicator of potential market trends, Volcano X urges caution in directly prejudging past patterns to predict future results, given the limited sample size of the previous three events.

現貨比特幣ETF在美國的推出從根本上改變了比特幣的供需格局。在成立後的兩個月內,這些ETF的淨流入額已達數十億美元,標誌著市場動態的重大轉變。這一發展不僅為BTC需求建立了新的基準,而且還表明即將到來的減半可能會對市場產生獨特的影響,與先前的週期不同。鑑於這些變化,了解當前的技術供需情況對於理解比特幣減半後的潛在情況至關重要。

In the two months since it was established, these ETF inflows have reached billions of dollars, marking a major shift in market dynamics. Not only has this development created a new baseline for BTC’s needs, but it also suggests that the forthcoming reduction could have a unique effect on the market, unlike in previous weeks.

儘管新比特幣供應的減少是一個需要考慮的關鍵因素,但它只是影響加密貨幣價值的眾多因素之一。自2020 年初以來,可用於交易的比特幣供應量(即流通和非流通供應量之間的差額)一直在下降,顯示與先前的週期相比發生了重大變化。然而,最近的數據顯示,自2023 年第四季初以來,活躍的BTC 供應量(在過去三個月內移動的比特幣)增加了130 萬,而同期新開採的比特幣僅增加了約15 萬個。儘管市場吸收這種供應的能力有所提高,但Volcano X建議不要過度簡化市場動態的複雜交互作用。

Although a reduction in the supply of new bits is a key factor to be considered, it is only one of many factors affecting the value of encrypted coins. Since the beginning of 2020, the amount of bitcoins available for trading (i.e., the difference between circulation and non-flow supply) has been declining, indicating a significant change from the previous period.

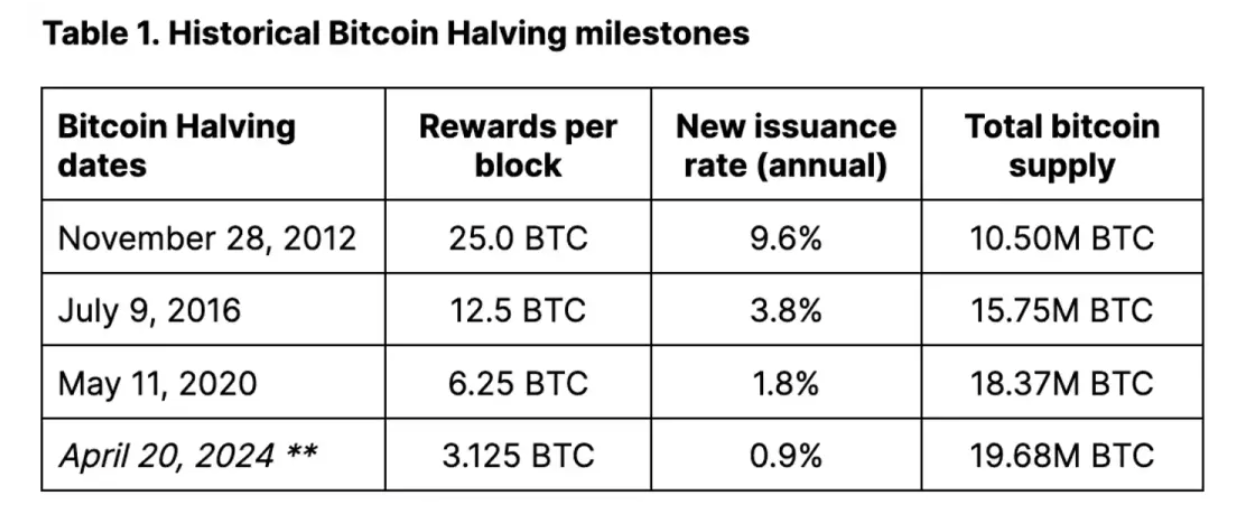

比特幣大約每四年減半一次,或每開採210,000 個區塊,有效地減少了礦工的獎勵,從而減少了新比特幣的每日發行量。減半後,比特幣的日產量預計將從約900個下降到450個,年通膨率從1.8%調整為0.9%。這些調整使比特幣的月產量達到約13,500個,年產量達到約164,250個,儘管這些數字 會受到實際哈希率的變化的影響。

會受到實際哈希率的變化的影響。

Bitcoins have been reduced by about half a year every four years, or by about 210,000 blocks per sector, effectively reducing the incentives for miners by reducing the daily turnover of new bitcoins. After that reduction, Bitcoins' daily output is expected to drop from about 900 to 450, with annual inflation adjusted from 1.8 per cent to 0.9 per cent. These adjustments have led to a change in the monthly production of bitcoins to about 13,500, while these figures

比特幣協議中嵌入的減半機制將持續到所有2,100 萬個比特幣被開採出來,這一事件預計將在2140 年左右發生。 Volcano X認為減半的潛在意義不僅在於其直接的市場影響,更在於它能夠吸引媒體對比特幣獨特屬性的高度關注:一個固定的、通貨緊縮的供應計劃,最終導致供應的硬性上限。比特幣的這一方面往往被低估了。

Volcano X believes that the potential for a half reduction is more than a direct market effect, and more so that it attracts media attention to the uniqueness of the Bitcoins: a fixed, tight supply plan that ultimately leads to a rigid ceiling on supply. This aspect of the Bitcoins is often underestimated.

對於有形商品,如礦產,理論上可以投入額外的資源來開採和提取更多的資源,如金或銅。儘管進入障礙可能很高,但價格上漲可以激勵滿足需求。然而,由於比特幣預設的區塊獎勵和難度調整機制,其供應量仍缺乏彈性(即對價格變化沒有反應)。此外,比特幣概括了一種成長敘事。比特幣網路的效用隨著網路上的用戶數量而擴大,直接影響代幣的價值。這與黃金等貴金屬形成鮮明對比,黃金沒有類似的成長預期。

For tangible goods, such as minerals, the theory is that additional resources can be invested to generate and extract additional resources, such as gold or copper. While barriers to entry may be high, price increases can stimulate demand. However, the supply is still less elastic (i.e., there is no response to price changes). The usefulness of the Bitcoins network increases with the number of users on the Internet, directly affecting the value of the money.

我們對比特幣表現的減半週期的分析本質上是有限的,因為之前只有三次發生。因此,對先前減半與比特幣價格之間的相關性的研究應該謹慎對待;樣本量小,因此僅根據歷史分析來模式化這些事件具有挑戰性。事實上,我們認為需要更多的減半週期,才能得出關於比特幣「通常」如何對減半做出反應的強烈結論。此外,相關性並不意味著因果關係,包括市場情緒、採用趨勢和宏觀經濟狀況在內的因素都可能導致價格波動。

Our analysis of the half-week drop in bitcoin performance is limited in nature, because it has only occurred three times before. Therefore, the study of the correlation between the previous half-bit dollar reduction and the price of bitcoin should be treated with caution; the sample is small, and it is therefore challenging to model these events only on the basis of historical analysis. In fact, we believe that more half-weeks are needed to draw strong conclusions about how bitcoin “normally” reacts to the reduction.

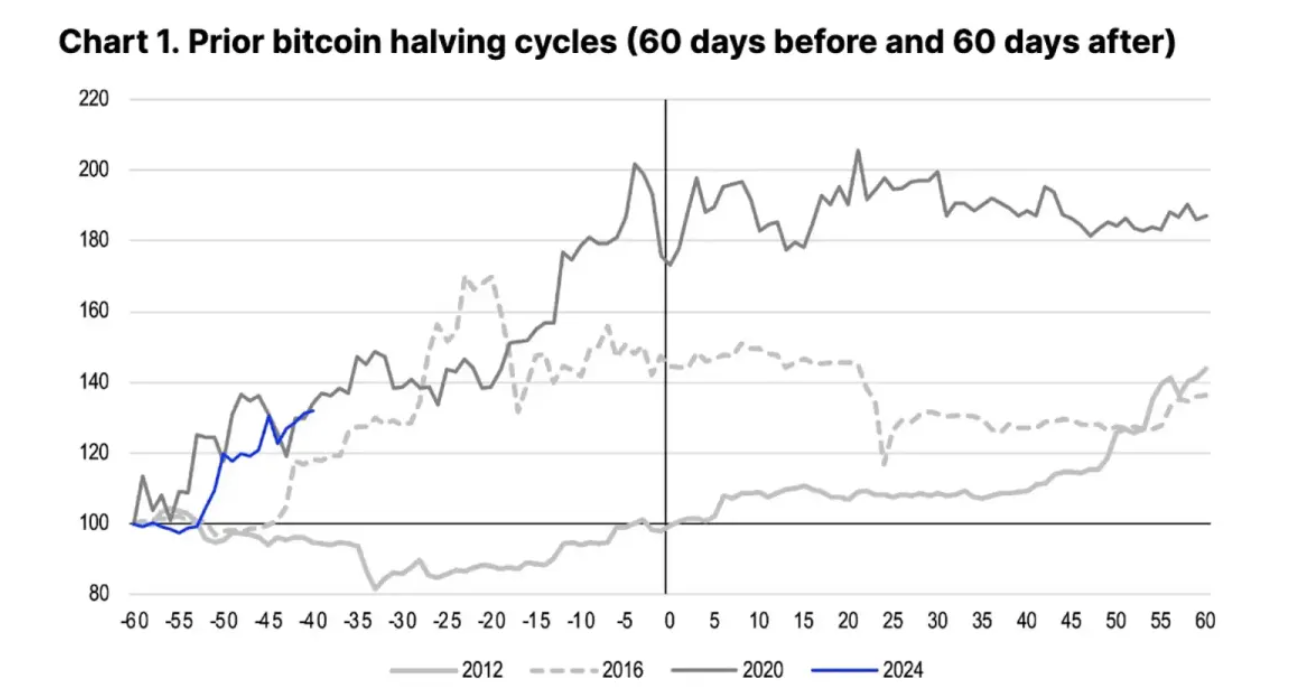

事實上,我們先前的假設是,比特幣在減半事件方面的表現取決於上下文,這可以解釋不同周期中價格軌蹟的顯著變化。如圖1 所示,比特幣的價格在2012 年11 月第一次減半之前的60 天內保持相對穩定,而在2016 年7 月和2020 年5 月第二次和第三次減半之前的同一時段內,比特幣的價格分別上漲了約45% 和73%。這種可變性凸顯了影響比特幣價格的因素之間的複雜相互作用,表明每個減半週期都在其獨特的背景框架內展開。

In fact, our previous assumption was that Bitcoin’s performance in reducing half the price was determined by the context, which explains the marked variation in price trajectory in different cycles. As figure 1 shows, Bitcoin prices remained stable for 60 days prior to the first halfdown in November 2012, while during the same periods in July 2016 and May 2020, during the second and third half reduction, the price of Bitcoins increased by about 45 per cent and 73 per cent respectively. This variability highlighted the complex interplay between factors affecting the price of the Bitcoat, suggesting that each half-week spread within its unique background framework.

在我們的分析中,第一次減半的有益影響直到2013年1月才完全顯現出來,當時聯準會量化寬鬆計畫(QE3)的影響與對美國債務上限危機的擔憂交織在一起。因此,我們認為,在普遍的通膨擔憂中,增加媒體對減半的報道可以提高大眾對比特幣作為替代價值儲存手段的認識。相較之下,在2016年,英國脫歐可能引發了英國和歐洲的金融焦慮,可能催化比特幣的購買行為。這種趨勢一直持續到2017年的ICO熱潮。 2020 年初,各國央行和政府 為因應COVID-19 大流行而採取前所未有的刺激措施,再次顯著提高了比特幣的流動性。

為因應COVID-19 大流行而採取前所未有的刺激措施,再次顯著提高了比特幣的流動性。

In our analysis, the beneficial impact of the first half has not been fully apparent until January 2013, when the impact of the QE3 campaign was combined with concerns about the US debt ceiling crisis. Thus, we believe that, in general inflation concerns, an increase in media coverage could raise public awareness of the Bitcoin as an alternative value saving tool. In contrast, in 2016, Britain’s financial anxiety could be triggered by Britain’s and Europe’s quantitative easing plan (QE3), which could trigger the purchase of the bitco. This trend continued until 2017’s ICO boom. At the beginning of 2020, central banks and governments

同樣重要的是要注意,對歷史表現的分析可能會因相對於減半事件的觀察期而有很大差異。無論分析著眼於從減半日期起30 天、60 天、90 天或120 天的時間段,價格回報指標都可能有所不同。因此,採用不同的窗口可能會影響從過去的價格表現中得出的結論。出於我們的目的,我們使用60 天的時間框架,因為它有助於過濾掉短期噪音,同時保持足夠接近減半,以便其他市場因素可能在長期內開始主導價格驅動因素。

It is also important to note that the analysis of historical performance may vary considerably as a result of a reduction in the period of observation of the event. Price feedback indicators may vary, regardless of the time period from 30 days, 60 days, 90 days, or 120 days from the date of the reduction. Therefore, the use of different windows may affect the conclusion drawn from past price performances. For our purposes, we use a 60-day time frame, as it helps to filter short-term noise and at the same time is close enough to the reduction, so that other market factors may begin to lead price drivers in the long run.

現貨比特幣ETF在美國的推出正在透過為比特幣需求建立新的基準來重塑比特幣的市場動態。在先前的周期中,流動性是價格上漲勢頭的關鍵障礙,因為主要市場參與者(包括但不限於比特幣礦工)會推動拋售,試圖退出多頭部位。現貨比特幣ETF的出現從根本上改變了這種動態,為機構和散戶投資者提供了一種更有條理和更容易獲得的方式來參與比特幣。

The introduction of the current Bitcoin ETF in the United States is creating a new basis for Bitcoin demand to re-establish the market dynamics of the bitcoins. In the previous cycle, mobility had been a key obstacle to rising prices, as major market players (including but not limited to the Bitcoins miners) would push for the sale and try to withdraw from multiple positions.

透過充當傳統金融和加密貨幣世界之間的橋樑,這些ETF緩解了先前看到的一些流動性問題,並擴大了投資者基礎。這種市場參與的多樣化不僅增強了流動性,而且有可能穩定與大規模拋售相關的價格波動。此外,ETF發行所隱含的機構支持賦予了比特幣一定程度的合法性,並鼓勵了比特幣的進一步採用。

Through the bridge between the traditional financial and encrypted currency worlds, these ETFs have eased some of the movement problems previously observed and have widened the investor base. This multiplicity of market participation has not only increased mobility, but also has the potential to stabilize price dynamics associated with large-scale sales. Moreover, the institutional support that ETF has hidden has given Bitcoins a degree of legitimacy and has encouraged further use of Bitcoins.

總而言之,以宏觀經濟因素、ETF等新興投資工具以及市場情緒變化為標誌的不斷變化的環境在塑造比特幣減半後的旅程中起著至關重要的作用。雖然歷史提供了寶貴的見解,但圍繞每個減半事件的獨特條件匯合意味著不能僅根據過去的趨勢來預測未來的結果。因此,利害關係人應將歷史知識和對當前發展的關注相結合,以接近市場。

All in all, the changing environment, marked by bold economic considerations, new investment instruments such as ETFs, and changing market moods, has played a crucial role in shaping the Bitt currency’s half-down. While history provides valuable insights, the unique combination of conditions around each half-down means that future results cannot be predicted solely on the basis of past trends.

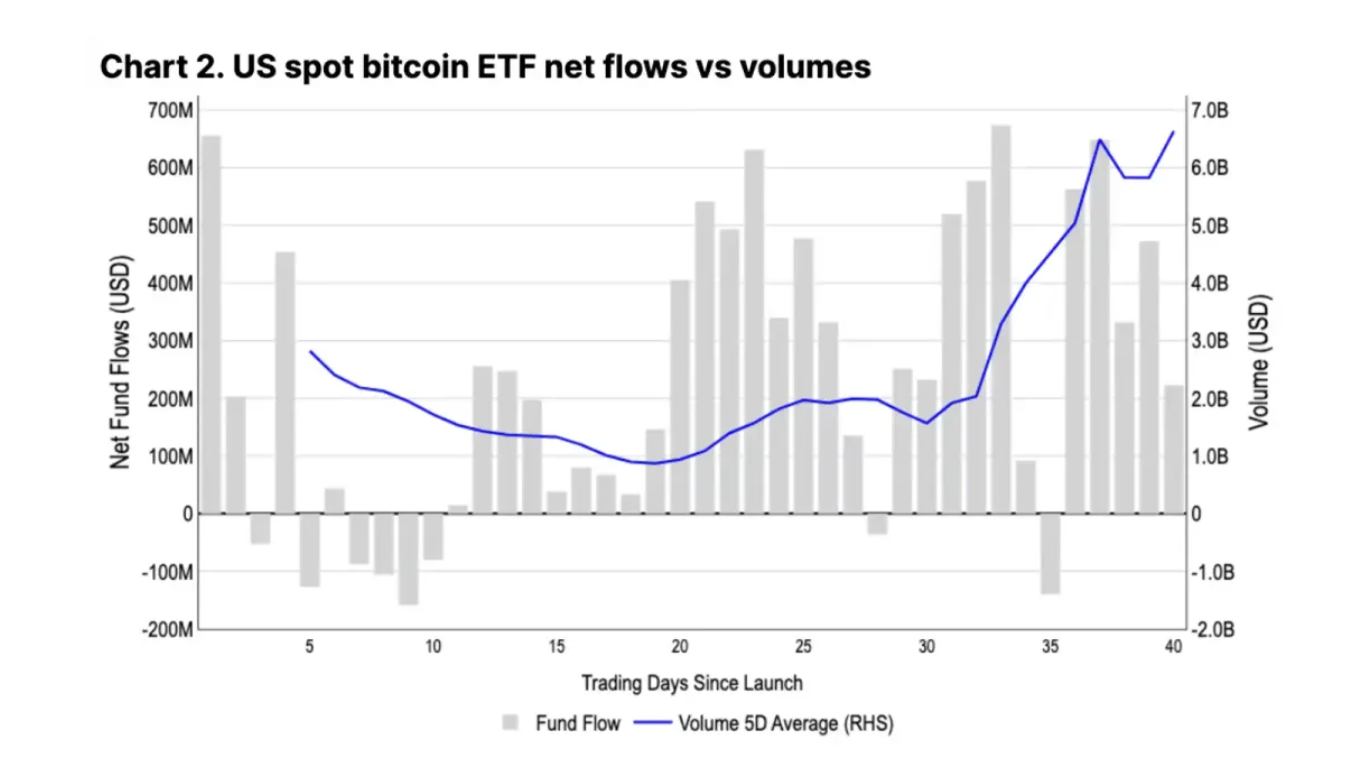

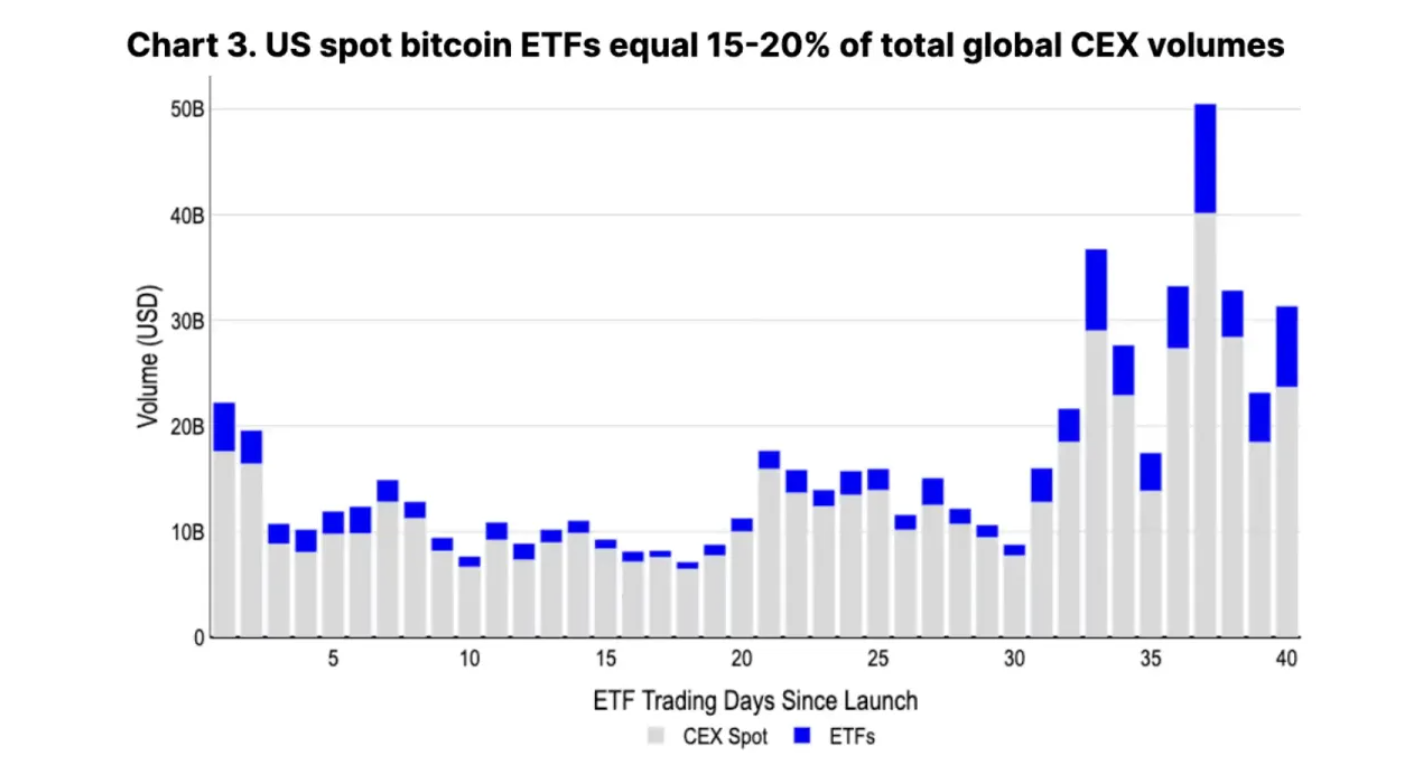

如今,流入ETF的資金有望以漸進和持續的方式吸收很大一部分供應。目前,ETF的BTC現貨日均交易量估計介於4-50億美元之間,佔全球中心化交易所總交易量的15-20%。這種流動性水準足以讓機構在該領域內輕鬆執行交易。從長遠來看,這種穩定的需求可能會對比特幣的價格產生正面影響,因為它可以促進一個更平衡的市場,減少集中拋售帶來的波動性。

Today, the flow of ETF funds is expected to absorb a large part of the supply in a gradual and sustained manner. Currently, the ETF’s BTC average daily turnover is estimated to be between $4 billion and $5 billion, accounting for 15 to 20% of the global centralized exchange total.

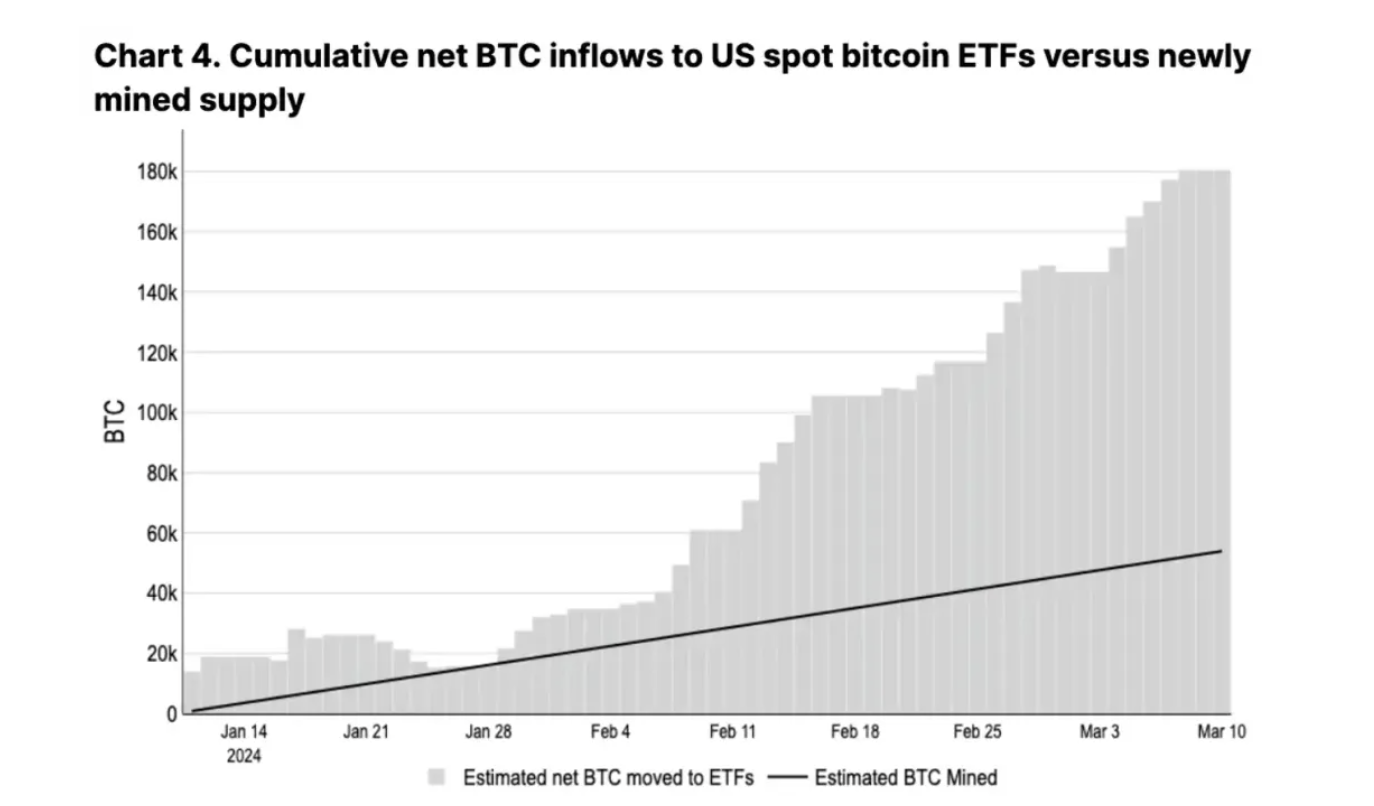

在推出後的前兩個月,美國的現貨比特幣ETF吸引了96億美元的淨流入,管理的總資產達550億美元。這項發展表明,在此期間,這些ETF(180,000個硬幣)持有的BTC的累積淨增長幾乎是礦工生產的55,000個新比特幣供應量的三倍(如圖3所示)。根據彭博社報道,縱觀全球所有現貨比特幣ETF的總和,這些受監管的投資工具目前持有約110萬枚比特幣,佔總流通供應量的5.8%。

In the first two months of the launch, the US current currency ETF attracted $9.6 billion in clean inflows, managing a total investment of $5.5 billion. This development shows that during this period, these ETFs (180,000 coins) held about three times the volume increase in BTC production of 55,000 new bits (as shown in figure 3). According to the Bloomberg News, these supervised investment instruments now hold about 1.1 million bits, accounting for 5.8 per cent of the total circulation supply.

從中期來看,我們可能會看到ETF保持甚至增加其目前的流動性水平,因為主要經紀交易商尚未開始向客戶提供這些產品。由於美國貨幣市場基金仍有超過6兆美元的資金,而且預期即將降息,我們相信,年內將有大量閒置資本流入這一資產類別。

In the medium term, we may see the ETF maintain or even increase its current liquidity levels, as the major dealers have not yet begun to supply their clients with these products. Since the US Monetary Market Fund still has more than $6 trillion in funds and is expected to cut interest rates, we are confident that there will be large amounts of idle capital flowing into this category in the course of the year.

值得一提的是,由於ETF 導致的比特幣持有集中化的潛在擔憂不會對網路構成穩定性風險,因為僅僅擁有比特幣不會影響去中心化網路或允許控制其節點。此外,金融機構目前無法提供基於這些ETF作為標的資產的衍生性商品。這種衍生性商品的可用性可能會改變大型參與者的市場結構。然而,保守估計,這些衍生性商品的監管批准可能還需要幾個月的時間。

It is worth mentioning that the potential concern of centralization of the bit currency caused by the ETF does not pose a stabilizing risk to the Internet, because mere possession of the bitcoins does not affect decentralizing the network or allow control of its nodes. Moreover, the financial institutions are currently unable to provide derivatives based on the ETF as a label. The availability of such derivatives may change the market structure of large players.

這一發展突顯了機構參與加密貨幣領域的重大轉變,這在一定程度上是由ETF的工具所推動的。隨著情勢的發展,傳統金融產品與比特幣等數位資產的整合不僅擴大了可及性,而且在市場流動性、投資者基礎擴張以及可能緩解價格波動方面引入了新的動力。不斷調整監管框架以適應這些創新,對於塑造比特幣的未來軌跡及其融入更廣泛的金融生態系統至關重要。

This development highlights the significant shift in institutional involvement in the domain of encryption currency, driven in part by ETF tools. As the situation unfolds, the integration of traditional financial products with digital assets such as Bitcoins has not only expanded in scope, but has also introduced new forces in market mobility, investor infrastructure expansion, and potentially price-resilient volatility.

This dynamic highlights the complex interplay between the supply and demand factors that influence the price of bits. Although miners do add new bits to the ecosystem, the broader context includes fluidity and non-movement supply changes, institutional use rates, and macro-economic trends. All of these factors help to shape the market environment for encrypted coins, complicating simple price prediction models based only on supply-side considerations.

乍一看,由於ETF的新機構需求,比特幣交易可用性的下降似乎是比特幣表現的主要技術支撐之一。然而,考慮到進入流通的新比特幣即將減少,這些供需動態表明潛在的短期市場收緊。也就是說,我們認為這個框架並不能完全捕捉到比特幣市場流動性動態的複雜性,特別是因為「非流動性供應」並不等於靜態供應。

At first glance, the decline in the availability of bitcoins seems to be one of the main technical support for bitcoins because of the new institutional needs of the ETF. However, considering that new bitcoins are about to be reduced into circulation, these supply and demand dynamics suggest potential short-term market tightening. That is, we do not think that this framework captures the full complexity of Bitcoins market dynamics, especially because "non-current supply" is not equivalent to static supply.

投資者不應忽視可能影響拋售壓力的幾個關鍵因素:

Investors should not lose sight of some of the key factors that may affect the pressure to sell:

- 並非所有在流動性缺口中佔比的比特幣都被「困住了」。與短期持有者相比,長期持有者(持有比特幣超過155 天,佔持有量的83.5%)可能對其部位的經濟敏感度較低。然而,我們預計隨著價格上漲,這群人中的一些人可能仍會選擇實現利潤。

- 一些持有者可能不打算在不久的將來出售,但仍然可以透過使用他們的比特幣作為抵押品來提供流動性。這也在一定程度上影響了這些比特幣的「非流動性」特性。

- 礦工可能會出售他們的比特幣儲備(目前在公共和私人礦工中總共有180萬BTC)以擴大他們的業務或支付其他成本。

- 短期持有者持有的約300萬BTC並非微不足道。在價格波動中,投機者仍可能退出以獲取利潤。

忽視這些重要的供應來源過於簡化了不可避免的稀缺性是由於採礦回報減少和ETF需求穩定而導致的論點。我們認為,需要進行更全面的評估,以確定即將到來的減半事件背後的真實供需動態。

Ignoring these important sources of supply is the argument that the inevitable scarcity is the result of reduced mining returns and stable ETF demand. We believe that a more comprehensive assessment is needed to determine the real supply and demand dynamics behind the upcoming half-lives.

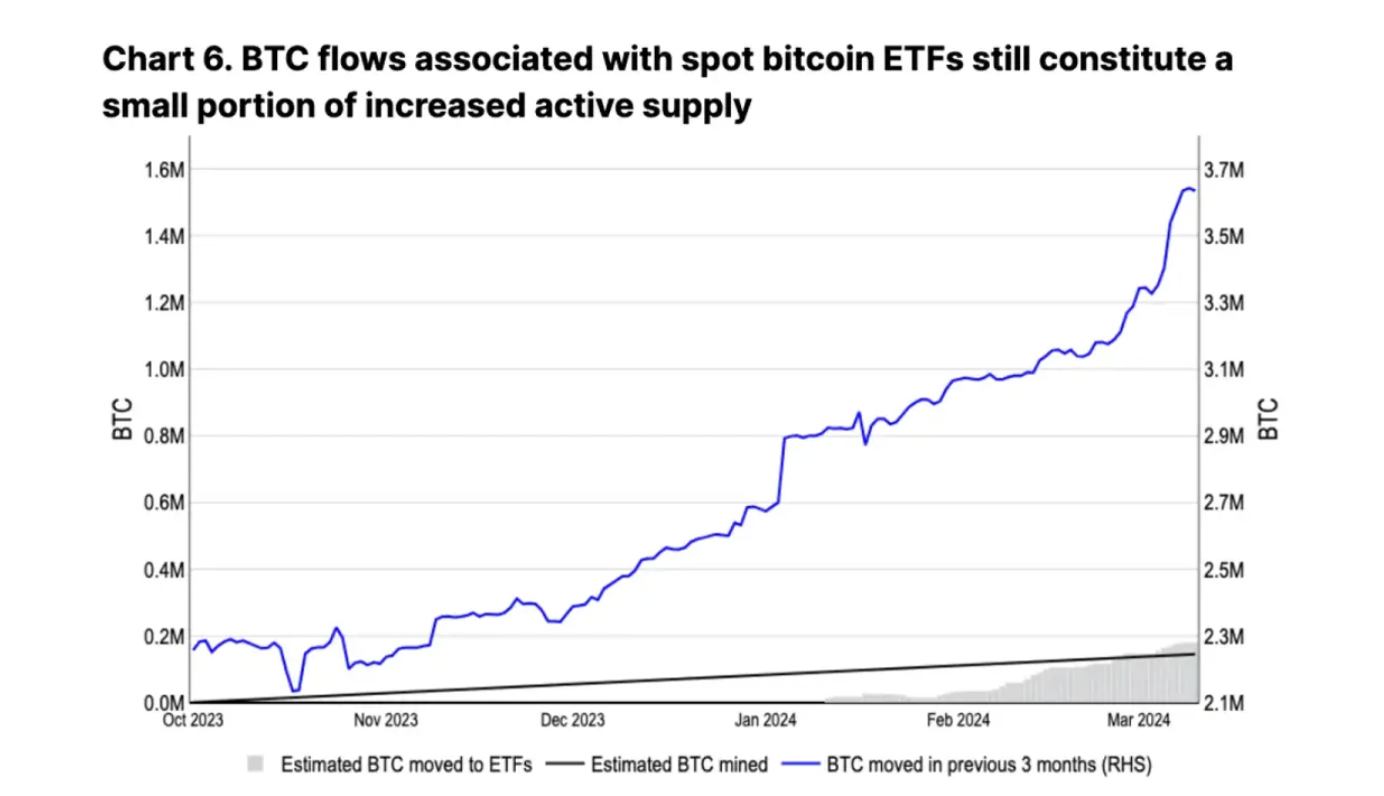

即使比特幣被納入ETF,活躍流通供應量(定義為過去3個月內轉移的比特幣)的成長率也大大超過了ETF的累積流入速度(如圖6所示)。自2023 年第四季以來,活躍的BTC 供應量增加了130 萬枚,而新開採的比特幣僅佔約15 萬枚。

Even if the bitcoins were included in the ETF, the rate of growth of the live circulation supply (defined as the bitcoins transferred in the last three months) is much higher than the rate of cumulative ETF inflows (as shown in figure 6). Since the fourth quarter of 2023, the live BTC supply has increased by 1.3 million, while the newly introduced bitcoins account for only about 150,000.

活躍供應的增加表明,儘管比特幣被吸收到ETF和其他長期持有策略中,但大量比特幣仍然具有流動性,並且是活躍交易週期的一部分。比特幣流動性的動態性質凸顯了對市場供應側以及各種因素(從礦工行為到投資者情緒)如何影響整體流動性格局的細緻入微的理解。

The increase in active supply suggests that even though bitcoins are absorbed into ETFs and other long-term holding strategies, large amounts of bitcoins are still fluid and are part of the active trading cycle. Bitcoins' dynamic dynamics highlight a slight understanding of how the market supply side and various factors (from mining industry to investor sentiment) influence the overall flow pattern.

此外,受宏觀經濟因素、技術進步和監管變化的影響,比特幣流動性的不斷變化將繼續影響其市場動態。因此,利害關係人必須保持警惕,調整其策略以應對這個複雜生態系統中預期和不可預見的變化。

In addition, subject to macro-economic factors, technological advances and regulatory changes, the constant evolution of the Bit currency flow will continue to affect its market dynamics. Stakeholders must therefore be vigilant and adjust their strategies to respond to anticipated and unpredictable changes in this complex system. 活躍供應的一部分確實來自礦工本身,他們可能會出售儲備以利用價格趨勢,並在收入減少的情況下建立流動性——我們在1 月30 日發布的報告《比特幣減半和礦工經濟學》中對此進行了更深入的討論。礦工的這種做法反映了他們在前幾個週期中的行為。然而,Glassnode 報告顯示,在2023 年10 月1 日至2024 年3 月11 日期間,礦工的錢包淨餘額僅減少了20,471 個比特幣,這表明新活躍的比特幣供應主要來自礦工以外的來源。 It is true that part of the supply comes from the miners themselves, who may sell reserves to take advantage of price trends and create liquidity in the face of reduced incomes — which we discussed in greater depth in our January 30 report, Bitcoins Half Down and Minerals Economics. This approach by miners reflects their behaviour during the previous weeks. However, Glasnode reports show that between October 1, 2023 and March 11, 2024, miners lost only 20,471 bits of their wallets, which suggests that the new biotech supply comes mainly from sources other than miners. 在先前的周期中,活躍供應的變化超過了新開採的比特幣的成長率的五倍以上。在2017 年和2021 年的週期中,活躍供應量幾乎翻了一番,在11 個月內分別增加了320 萬(從低潮增加到610 萬),在7 個月內增加了230 萬(從310萬增加到540 萬)。相較之下,在同一時期開採的比特幣數量分別約為600,000 和200,000。 During the previous cycle, living supply changed more than five times the growth rate of newly introduced bitcoins. During the rest of 2017 and 2021, living supply almost doubled, increasing by 3.2 million (from low tide to 6.1 million) in 11 months, and 2.3 million (from 3.1 million to 5.4 million) in seven months. In contrast, the number of bitcoins in the same period increased by about 600,000 and 200,000. 同時,在這個週期中,比特幣的非活躍供應量(定義為比特幣超過一年不變)也連續三個月下降,這可能意味著長期持有者開始拋售(如圖7 所示)。在正常情況下,這將被解釋為週期中期訊號。在2017 年和2021 年的週期中,從非活躍供應達到高峰到達到週期最高價格的時間跨度分別約為12 個月和13 個月。當前週期中非活躍比特幣的峰值似乎在2023 年12 月達到。 At the same time, the non-living supply of bitcoins (defined as bitcoins for more than a year) has also declined for three consecutive months during this period, which may mean that long-term holders are starting to sell (as figure 7 shows). Under normal circumstances, this will be interpreted as a medium-term signal of the week. In the weeks of 2017 and 2021, the length of time between the peak of the non-living supply and the peak of the period is about 12 months and 13 months. 長期持有者和礦工的市場活動可能增加,加上機構需求透過ETF的動態湧入,凸顯了比特幣供需方程式的多面性。活躍和非活躍供應之間的相互作用為市場情緒和潛在的未來價格趨勢提供了寶貴的見解。 The potential increase in the market activity of long-term holders and miners, coupled with institutional demand through the dynamism of the ETF, highlights the multi-faceted nature of bitcoin supply and demand equations. The interaction between active and non-living supply provides valuable insight into market sentiment and potential future price trends. 鑑於這些觀察結果,比特幣生態系統中的利害關係人應密切注意這些供應動態,因為它們可以提供有關市場方向變化的早期訊號。此外,了解不同市場參與者(包括礦工、長期持有者和機構投資者)的行為有助於在這個複雜且不斷變化的環境中做出明智的決策。 As a result of these observations, stakeholders in the Bitcoin ecosystem should pay close attention to these supply dynamics because they can provide early signals about market direction changes. Moreover, understanding the behaviour of different market participants (including miners, long-term holders and institutional investors) can help to make informed decisions in this complex and constantly changing environment. 當我們在Volcano X基金公司分析比特幣的演變格局及其與主流金融工具的整合時,很明顯,與以前的周期相比,這個週期提供了獨特的動力。美國現貨比特幣ETF的引入和持續的每日淨流入代表了一個巨大的推動力,標誌著機構對數位資產的廣泛接受和投資發生了顯著轉變。 When we analyse the evolution of the bitcoins and their integration with mainstream financial instruments at Volcano X, it is clear that this week provides a unique momentum compared to the previous cycle. The introduction and continued daily net influx of the US current bitcoins ETF represents a huge push, marked by a marked shift in the broad acceptance and investment of digital assets by institutions. 考慮到減半事件導致的新比特幣供應即將減少,我們觀察到市場動態收緊,這可能會改變傳統的供需平衡。雖然有些人可能會猜測將進入供應緊縮,但我們的分析表明,未來需求和拋售壓力將需要找到新的平衡。 Considering the reduction in the new bitcoin supply as a result of the half event, we observe a tightening of market dynamics, which may change the traditional balance between supply and demand. While some may suspect that supply will become tight, our analysis suggests that future demand and selling pressure will need to find a new balance. 現貨比特幣ETF的作用怎麼強調都不為過。作為一種新的資產類別,這些ETF彌合了傳統投資策略與數位資產領域之間的差距,標誌著比特幣主流採用的關鍵時刻。這項發展不僅增強了比特幣作為可投資資產的流動性和穩定性,也為傳統投資者在受監管的框架內參與加密貨幣市場開闢了途徑。 As a new asset category, these ETFs bridge the gap between traditional investment strategies and digital domains, marking the key moment in the mainstream of the Bitcoins. This development not only enhances the mobility and stability of the Bitcoins as an investmentable asset, but also opens the way for traditional investors to participate in the encryption currency market within a regulated framework. 此外,我們的研究顯示,圍繞比特幣流動性和供應動態的敘述遠比乍看複雜得多。休眠供應變得活躍、礦工行為以及衍生性商品放大現貨市場活動的影響之間的相互作用凸顯了比特幣市場生態系統的多面性。 Moreover, our research shows that the narratives surrounding the currency flow and supply dynamics are much more complicated than first glances. The interplay between dormant supply becoming active, mining behaviour, and derivatives magnifying the impact of current market activity highlights the multi-faceted nature of the Bitcoin system. 鑑於這些見解,Volcano X對比特幣的前景保持謹慎樂觀。我們斷言,雖然存在與供需相關的直接障礙,但發生的基本性轉變——主要是透過ETF將比特幣制度化——預示著其長期發展軌跡。因此,我們認為,目前的趨勢表明,可能長期的牛市階段才剛開始,需要不斷調整市場動態,以促進供需之間的可持續平衡。 Given these observations, Volcano X is cautiously optimistic about the future of the bitcoins. We say that, although there are direct barriers to supply and demand, the fundamental shifts that have taken place – mainly through the institutionalization of the bitcoins through the ETF – are indicative of their long-term course of development. 總之,作為我們為客戶和合作夥伴提供前瞻性分析的承諾的一部分,Volcano X將繼續密切關注這些發展。我們的目標是策略性地駕馭這些變化,確保我們處於有利地位,以利用比特幣進一步鞏固其在全球金融格局中的地位所出現的機會。 In short, as part of our commitment to provide forward-looking analysis for clients and partners, Volcano X will continue to follow these developments closely. Our goal is to strategically drive these changes to ensure that we are in a position to take advantage of the opportunities presented by the Bitcoins to further entrench their position in the global financial landscape. 免責聲明:本文件僅供參考與交流之用,不構成投資建議。 Exemption statement : This document is intended for reference and communication purposes only and does not constitute investment advice. 圖片來源: Image source:

注册有任何问题请添加 微信:MVIP619 拉你进入群

打开微信扫一扫

添加客服

进入交流群

发表评论